Form 5471 master guide: complete IRS filing reference for 2026

A six part Form 5471 guide built entirely from IRS instructions, the Internal Revenue Code, and Treasury Regulations. Filing categories, CFC ownership, Subpart F, NCTI, penalties, and more.

5471 GUIDE

7/12/20264 min read

Form 5471 sits at the center of nearly every cross border business structure a U.S. person controls, owns, or acquires an interest in, and it is one of the least forgiving forms in the entire tax code. The penalties are severe and can apply even where no additional U.S. tax is due, the categories of filer overlap in ways that trip up experienced practitioners, and the underlying law changed materially under the 2025 One Big Beautiful Bill Act. Guidance that has not caught up with that legislation is now actively wrong in places.

This guide works through Form 5471 in six parts, built only from primary sources: the IRS instructions to Form 5471 (revised December 2025), the Internal Revenue Code sections the form implements, the Treasury Regulations that define its key terms, and the named revenue procedures the instructions themselves point to. Each part is fact checked against those sources before publication. Where the OBBBA changed something, that change is flagged rather than left buried in outdated terminology.

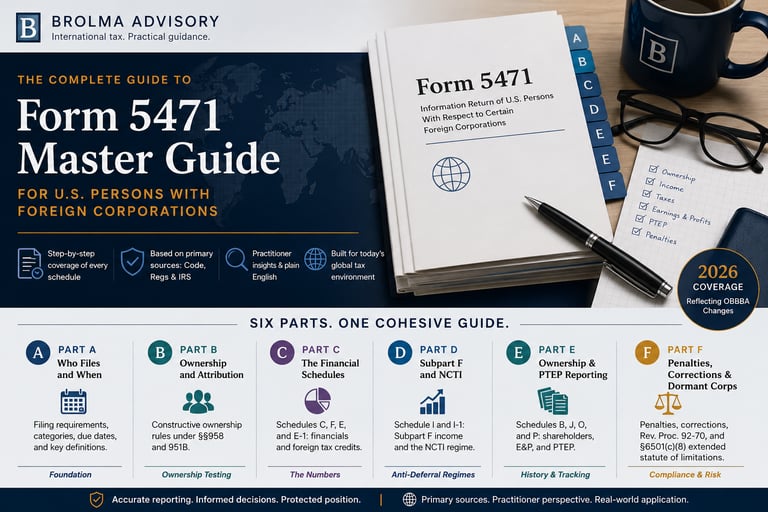

What each part covers

Part A: Who must file and when

The foundation the rest of the form sits on. Covers the five categories of filer (1 through 5, including the 1a/1b/1c and 5a/5b/5c sub types), the ownership and control thresholds that trigger each category, the exceptions that excuse otherwise qualifying filers, the joint filing rules, and when and where the form actually gets submitted.

Part B: Constructive ownership and CFC status

Goes underneath the filing categories to the attribution mechanics themselves. Covers the section 958(a) and (b) constructive ownership rules, how Treasury Regulations section 1.958-2 applies them, the full definitions of controlled foreign corporation under section 957 and U.S. shareholder under section 951, and how downward attribution actually pulls foreign owned U.S. entities into CFC status.

Part C: The financial schedules

A working guide to Schedules C, F, E, and E-1, the income statement, balance sheet, and foreign tax credit mechanics that most of the form's numerical reporting runs through. Covers how amounts get translated into U.S. dollars, the divide by convention for exchange rates, and how foreign taxes paid or accrued get allocated and tracked.

Covers Schedule I and Schedule I-1, the historic Subpart F income categories, and the regime formerly known as GILTI, renamed Net CFC Tested Income (NCTI) under the OBBBA for tax years beginning after December 31, 2025. Includes the removal of the QBAI carveout, the revised section 250 deduction percentages, and how the two regimes interact without double counting.

Part E: Ownership and transaction reporting

Covers Schedule B (shareholder identification), Schedule J (accumulated earnings and profits), Schedule O (organizations, reorganizations, and stock acquisitions or dispositions), and Schedule P (previously taxed earnings and profits, or PTEP). This is where most of the form's transaction history and ownership tracking lives.

Part F: Penalties, corrections, and dormant corporations

Covers the section 6038 and 6046 penalty structure, the criminal penalties under sections 7203, 7206, and 7207, the correction process for a wrong or incomplete filing, the summary filing procedure available for dormant foreign corporations under Rev. Proc. 92-70, and the extended statute of limitations under section 6501(c)(8) for incomplete or unfiled international information returns.

About Brolma Advisory

Brolma Advisory is an accounting, tax, and financial advisory firm built for businesses and individuals whose situations do not fit standard templates. We work with international businesses establishing or operating in the United States, US companies expanding abroad, and complex businesses including SEC reporting and public company close support, multi-entity and intercompany structures, tech and SaaS platforms, subscription and recurring revenue models, and e-commerce and platform sellers. On the individual side, we advise UK and US professionals, founders, and investors navigating both tax systems, along with US expats living and working abroad.

What connects all of it is complexity that generic accounting was never built to handle. Cross border ownership, deferred revenue, multi-currency reporting, entities with non-US owners, cash and revenue that never quite line up. Brolma Advisory builds accounting and tax structures that reflect how these businesses actually work, so the numbers make sense and the compliance holds up wherever it is tested.

Form 5471 master guide: complete IRS filing reference for 2026, by Brolma Advisory

A six part Form 5471 guide built entirely from IRS instructions, the Internal Revenue Code, and Treasury Regulations. Filing categories, CFC ownership, Subpart F, NCTI, penalties, and more.

Part A: Who must file and when

Part B: Constructive ownership and CFC status

Part C: The financial schedules

Disclaimer:

Content published by Brolma Advisory is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Brolma Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@brolma.com

Brolma Advisory

941 W Morse Blvd suite 100

Winter Park

Florida

32789