Form 5471 master guide: filing requirements 2026 - Who must file and why

A complete breakdown of who must file Form 5471, the five filer categories, and the filing exceptions, sourced directly from IRS instructions. Part 1 of the Brolma Advisory Form 5471 Master Guide.

5471 GUIDE

7/13/202612 min read

Form 5471 master guide, part 1: Who must file and when

Form 5471 is one of the most consequential information returns in international tax. It looks like a form. In practice it is a compliance regime, built on top of decades of code sections, revenue procedures, and layered category definitions that were never designed to be read by anyone outside the IRS Office of Chief Counsel. Practitioners avoid it, clients fear it, and the penalties for getting it wrong are severe and can apply even where no additional U.S. tax is due.

This is the first part of a multi part series that works through Form 5471 using only primary IRS sources: the form instructions themselves (revised December 2025), the underlying Internal Revenue Code sections, the Treasury Regulations, and the named revenue procedures the instructions point to. Nothing here comes from a summary of a summary. Where the law changed under the One Big Beautiful Bill Act (OBBBA, Public Law 119-21, enacted July 4, 2025), that is flagged explicitly rather than left for you to discover later.

A note before we start: the penalties are severe and can apply even when no additional U.S. tax is owed, but they are not without any defense. Reasonable cause relief exists under section 6038(c)(4), and the instructions themselves reference alleviation in certain cases under Regulations sections 1.6038-1(j)(4) and 1.6038-2(k)(3). Part F of this series covers the penalty structure and the available relief in full.

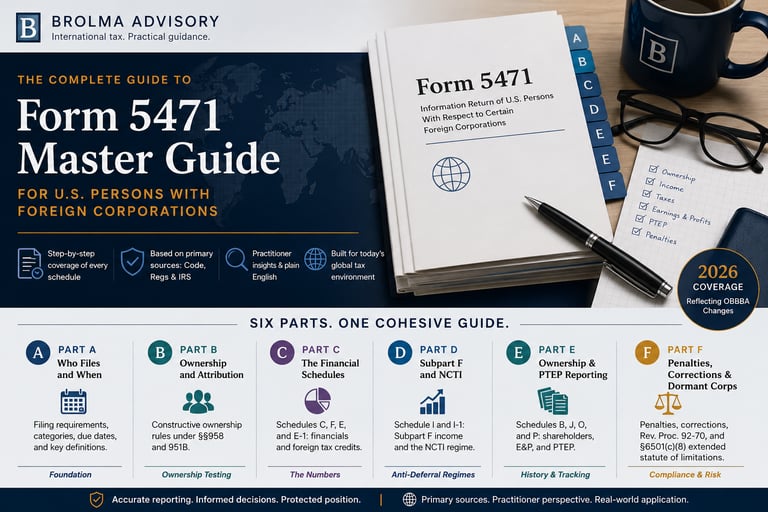

Part 1 covers the foundation everything else depends on: who has to file, the five categories of filer, the exceptions that let some people off the hook, and when and where the form gets filed.

What the form actually does

Form 5471 exists to satisfy two separate reporting requirements in the Internal Revenue Code: section 6038, which requires certain U.S. persons to report information about foreign business entities they control or have an interest in, and section 6046, which requires reporting of organizations, reorganizations, and acquisitions involving foreign corporations. The form and its schedules are the IRS’s chosen vehicle for meeting both requirements at once, for officers, directors, and shareholders connected to certain foreign corporations.

A foundational rule that trips people up immediately: a separate Form 5471, with all applicable schedules, must be filed for each foreign corporation. You do not consolidate multiple foreign corporations onto one form. If a client has three foreign subsidiaries, that is three separate Forms 5471, even if the filer and the filing category are identical across all three.

A second foundational rule: even when every dollar amount on a required schedule is zero, the schedule still has to be filed. Silence is not an option. For schedules completed by category rather than by corporation (Schedules E, I-1, J, P, and Q), including one instance of the schedule for any separate income category satisfies the requirement.

The five categories of filer

Everything about what you have to complete on Form 5471 flows from which category or categories describe the person filing. Get the category wrong and you will either over file or, worse, under file and expose the client to penalties. There are five numbered categories, and three of them split further into lettered sub categories.

Category 1: U.S. shareholders of a section 965 specified foreign corporation

A Category 1 filer is a U.S. shareholder of a foreign corporation that was a section 965 specified foreign corporation (SFC) at any point during the foreign corporation’s tax year, who also owned that stock on the last day the corporation held SFC status during that year.

For this category, a U.S. shareholder is a U.S. person who owns, directly, indirectly, or constructively under section 958(a) and (b), 10% or more of the combined voting power or value of the SFC’s stock. A U.S. person, for these purposes, is a citizen or resident of the United States, a domestic partnership, a domestic corporation, or a non foreign estate or trust.

A section 965 SFC is either a controlled foreign corporation (CFC, defined under Category 5 below) or any foreign corporation in which one or more domestic corporations are U.S. shareholders. A passive foreign investment company that is not a CFC falls outside this definition.

Category 1 splits into three sub types:

• Category 1a: a Category 1 filer who is not a 1b or 1c filer. This is the default.

• Category 1b: an unrelated section 958(a) U.S. shareholder of a foreign controlled section 965 SFC. In plain terms, this is someone who directly or indirectly owns stock in the SFC under section 958(a) but is not related to it under the section 954(d)(3) attribution rules.

• Category 1c: a related constructive U.S. shareholder of a foreign controlled section 965 SFC. This is the mirror image of 1b: someone who does not own stock under section 958(a) but is related to the SFC and picks up a filing obligation purely through constructive ownership.

A foreign controlled section 965 SFC is a foreign corporation that would not qualify as an SFC at all if you stripped out the downward attribution rules in section 318(a)(3)(A) through (C), the rules that let a foreign parent’s ownership be attributed down to a U.S. subsidiary for CFC testing purposes.

Category 1 reporting does not end just because the triggering event passed. A Category 1 filer must keep filing as long as the SFC has accumulated section 965 earnings and profits reportable on Schedule J, or the filer personally has previously taxed earnings and profits related to section 965 reportable on Schedule P.

Category 2: officers and directors present at a 10% acquisition

Category 2 covers a U.S. citizen or resident who is an officer or director of a foreign corporation at the time a U.S. person acquires either enough stock to cross the 10% ownership threshold, or an additional 10% or more of value or voting power on top of an existing position.

The 10% threshold, for this category, means 10% or more of total value or 10% or more of total combined voting power of stock with voting rights. Acquisition includes situations where the U.S. person has an unqualified right to receive the stock, even before it is formally issued.

Category 2 filers who are shareholders, officers, or directors of a foreign sales corporation (a legacy structure under former section 922) also need to attach a separate Schedule O to report ownership changes.

Category 3: acquirers, dispositions, and threshold crossings

Category 3 is the broadest trigger category. It picks up a U.S. person who:

1. Acquires stock that, combined with stock already owned, causes total ownership to meet the 10% ownership threshold

2. Acquires a new block of stock that itself meets the 10% ownership threshold, regardless of how much stock was already owned before that acquisition (this is what catches someone who already owns 20% and buys another 10% block)

3. Is treated as a U.S. shareholder under section 953(c) with respect to the corporation

4. Becomes a U.S. person while already meeting the 10% threshold

5. Disposes of enough stock to drop below the 10% threshold

Category 3 filers carry an extra burden: a required statement disclosing the amount and type of any indebtedness the foreign corporation holds with related persons under Regulations section 1.6046-1(b)(11), plus the name, address, identifying number, and share count for every subscriber to the corporation’s stock.

Category 4: control

Category 4 is the category most people associate with Form 5471, and it is defined by control rather than a percentage threshold alone. A U.S. person has control of a foreign corporation if, at any point during that person’s tax year, they own stock representing more than 50% of total combined voting power, or more than 50% of total value.

Control also reaches through chains of ownership. If a person controls a corporation that in turn owns more than 50% of another corporation’s voting power or value, that person is treated as controlling the second corporation too. The instructions give a clean four link example: Corporation A owns 51% of B, B owns 51% of C, C owns 51% of D. A controls D, even though A has no direct stake in D at all.

Category 4’s definition of U.S. person is broader than the other categories. It includes citizens and residents, nonresident aliens who have made a section 6013(g) election to be treated as a resident, and certain nonresident aliens covered by the section 6013(h) election for individuals who become residents mid year and are married to a citizen or resident at year end, in addition to domestic partnerships, domestic corporations, and non foreign estates and trusts.

Category 5: U.S. shareholders of a CFC

Category 5 is the CFC equivalent of Category 1’s SFC framework, and it is the category most cross border business owners fall into once their foreign entity is genuinely controlled from the U.S. side.

A Category 5 filer is a U.S. shareholder who owned stock in a foreign corporation that was a CFC at any point during the corporation’s tax year, and who held that stock on the last day it was a CFC during that year.

A CFC, in general, is a foreign corporation where U.S. shareholders own, directly, indirectly, or constructively under section 958(a) and (b), more than 50% of either total combined voting power of voting stock or total value of stock, on any day of the corporation’s tax year. There are narrower CFC definitions that apply specifically for insurance income and related person insurance income purposes under sections 957(b) and 953(c)(1)(B), but the general voting power or value test is what most practitioners will use.

Category 5 splits the same way Category 1 does:

• Category 5a: the default, anyone who is a Category 5 filer but not 5b or 5c.

• Category 5b: an unrelated section 958(a) U.S. shareholder of a foreign controlled CFC, someone who owns the stock directly or indirectly but is not related to the CFC under section 954(d)(3).

• Category 5c: a related constructive U.S. shareholder of a foreign controlled CFC, someone who does not own the stock under section 958(a) but is related to the CFC.

The instructions include a genuinely useful worked example here. U, a domestic corporation, owns 15% of FP, a foreign corporation. FP wholly owns D, a domestic corporation, and FS, a foreign corporation. FS is a foreign controlled CFC because it would not be a CFC at all without the downward attribution rules pulling D’s deemed ownership into the count. U is a Category 5b filer, since it indirectly owns FS stock and is not related to FS. D is a Category 5c filer, since it only owns FS constructively through FP and is related to FS. Critically, U and D cannot file a joint Form 5471 together, because 5b and 5c filers do not share the same filing requirements.

Exceptions that apply across nearly every category

The instructions carve out several situations where a filer who technically falls into a category does not have to file. Two exceptions show up repeatedly, but they do not cover the same categories, so it matters which one you are reaching for.

Constructive ownership through another filer, all categories. If you do not own a direct interest in the foreign corporation, your filing obligation exists solely because of constructive ownership attributed from another U.S. person, and that other person files a Form 5471 covering all the information your category would otherwise require, you are excused. This version is available to Categories 1, 2, 3, 4, and 5, though the exact wording and cross referenced regulations differ slightly by category. No attached statement is needed to claim it.

Constructive ownership from a nonresident alien, Categories 1, 4, and 5 only. If you have no direct or indirect interest in the foreign corporation and your only filing trigger is constructive ownership from a nonresident alien, you are excused, again without an attached statement. This exception does not extend to Category 2 or Category 3. A Category 2 or 3 filer whose only connection runs through a nonresident alien cannot rely on this provision.

Category 2’s additional relief. A Category 2 filer is also excused if, immediately after the acquisition, three or fewer U.S. persons own 95% or more in value of the foreign corporation’s stock and the acquiring U.S. person reports the acquisition as a Category 3 filer instead.

No section 958(a) U.S. shareholder (Categories 1 and 5 only). If no U.S. shareholder, including you, owns stock under section 958(a) in a foreign controlled SFC or CFC on the last relevant day, you are excused. This extends relief originally announced for Category 5 filers in Notice 2018-13 to the equivalent Category 1 situation.

Unrelated constructive U.S. shareholder (Categories 1 and 5 only). If the corporation is foreign controlled, you do not own stock in it under section 958(a), and you are not related to it under section 954(d)(3), you are excused. This implements relief from section 8.04 of Rev. Proc. 2019-40.

Two further exceptions apply broadly regardless of category:

Joint filing. One person can file Form 5471 on behalf of others describing the same foreign corporation for the same period, as long as that person’s filing requirements are equal to or greater than the others. A Category 5 filer, for instance, can file jointly with a Category 4 filer. The exception that breaks this: Category 5b and 5c filers can never file jointly with each other, because their required schedules diverge. Category 3 filers can only piggyback on someone with an equal or greater ownership interest.

Domestic corporations with a section 953(d) election. Shareholders of a foreign insurance company that has elected under section 953(d) to be treated as a domestic corporation, and that files a U.S. income tax return on that basis, do not need to file Form 5471 for it.

What gets filed, by category, at a glance

The filing requirement table in the instructions is dense, so treat this as an orientation and check the table itself against your specific category before relying on it. Categories 3 and 4 are the only ones that complete Schedule A and Schedule B Part I. Category 3 also completes Schedule B Part II, Schedules C and F, Schedule G, separate Schedule G-1, and separate Schedule O Part II, on top of the related party debt and subscriber statement described above. That is a longer list than Schedule O Part II on its own.

Category 4 and Category 5a carry the heaviest reporting burdens overall, and their requirements largely overlap: separate Schedules E, E-1, G, G-1, H, H-1 (where CAMT applies), I, I-1, J, P, Q, and R. They are not identical, though. Schedule M is a Category 4 requirement only; Category 5a does not complete it.

Category 2 files only Schedule O Part I, alongside the identifying information every category completes. The 1b, 1c, 5b, and 5c sub categories generally pick up a narrower slice of Schedule E, E-1, G, G-1, and P, often conditioned on whether the filer is claiming deemed paid foreign tax credits.

Two identifying rules matter regardless of category. First, if you meet the tests for both Category 4 and Category 5a, only check the Category 4 box and leave 5a blank. Second, if you are filing on behalf of others under the joint filing exception, only check the categories that describe you personally.

When and where to file

Form 5471 is not filed as a standalone submission. It attaches to the filer’s income tax return, or partnership or exempt organization return where applicable, and is due on the same schedule as that return, including any extensions actually claimed. There is no separate Form 5471 deadline to track independently of the underlying return, but there is also no independent extension available if the underlying return does not get one.

If a previously filed Form 5471 turns out to be incomplete or wrong, the fix is a corrected form attached to an amended return, with “Corrected” written at the top and a statement identifying exactly what changed. There is no separate standalone amendment process.

A note on what changed under OBBBA

The category definitions and required schedules described above come straight from the December 2025 instructions and reflect current law as written. But two 2025 legislative changes sit underneath these categories and can change who actually lands in them, for foreign corporation tax years beginning after December 31, 2025. OBBBA restored section 958(b)(4), reversing a 2017 repeal that had been pulling foreign corporations into CFC status through downward attribution alone with no real change in control, and added a new, narrower anti-abuse rule at section 951B. Part B of this series covers both in full. Separately, CFC tax years can no longer begin one month ahead of the majority U.S. shareholder’s year for tax years beginning after November 30, 2025, and a new Pro Rata Share Transition Rule affects how certain CFC dividends interact with section 951(a)(2)(B).

Sections 958(b)(4) and 951B are new law without implementing regulations or updated form instructions behind them yet. Check for further IRS guidance before relying on this framework for a tax year beginning after December 31, 2025.

Coming up in part 2

Part 2 goes underneath the filing categories to the mechanics of ownership itself: the constructive ownership attribution rules under section 958 and Treasury Regulations section 1.958-2, and the full CFC and U.S. shareholder definitions under sections 957 and 951, including how the downward attribution rules actually work in practice.

Sources for this article: IRS Instructions for Form 5471 (Rev. 12/2025); IRC §§6038, 6038(a), 6038(c)(4), 6046, 951B, 953(c), 953(d), 954(d)(3), 958(a)-(b), 965; Treasury Regulations §§1.6038-1(j)(4), 1.6038-2, 1.6038-2(k)(3), 1.6046-1; Notice 2018-13, 2018-6 I.R.B. 341; Rev. Proc. 2019-40, 2019-43 I.R.B. 982; One Big Beautiful Bill Act, Public Law 119-21 (July 4, 2025).

Form 5471 master guide: complete IRS filing reference for 2026, by Brolma Advisory

A six part Form 5471 guide built entirely from IRS instructions, the Internal Revenue Code, and Treasury Regulations. Filing categories, CFC ownership, Subpart F, NCTI, penalties, and more.

Part A: Who must file and when

Part B: Constructive ownership and CFC status

Part C: The financial schedules

About Brolma Advisory

Brolma Advisory is an accounting, tax, and financial advisory firm built for businesses and individuals whose situations do not fit standard templates. We work with international businesses establishing or operating in the United States, US companies expanding abroad, and complex businesses including SEC reporting and public company close support, multi-entity and intercompany structures, tech and SaaS platforms, subscription and recurring revenue models, and e-commerce and platform sellers. On the individual side, we advise UK and US professionals, founders, and investors navigating both tax systems, along with US expats living and working abroad.

What connects all of it is complexity that generic accounting was never built to handle. Cross border ownership, deferred revenue, multi-currency reporting, entities with non-US owners, cash and revenue that never quite line up. Brolma Advisory builds accounting and tax structures that reflect how these businesses actually work, so the numbers make sense and the compliance holds up wherever it is tested.

Disclaimer:

Content published by Brolma Advisory is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Brolma Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@brolma.com

Brolma Advisory

941 W Morse Blvd suite 100

Winter Park

Florida

32789