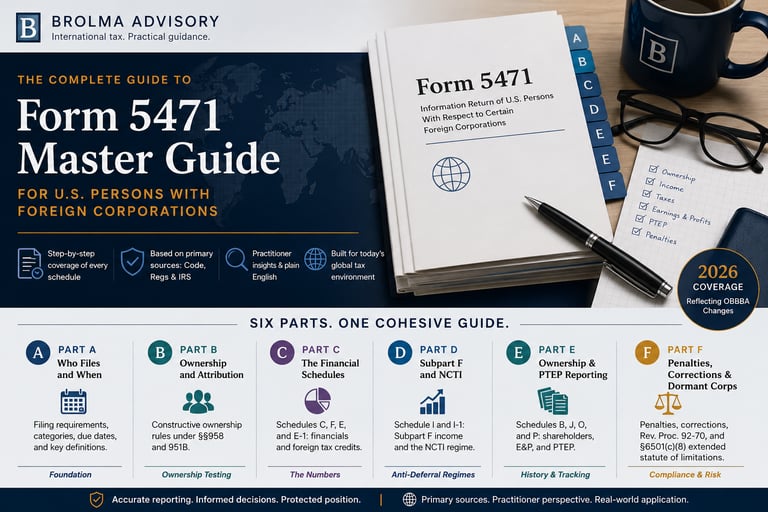

Form 5471 master guide: Form 5471 ownership and PTEP reporting guide

How Schedules B, J, O, and P track shareholder changes, earnings and profits, and previously taxed income on Form 5471. Part E of the Brolma Advisory Form 5471 Master Guide.

5471 GUIDE

7/17/20266 min read

Form 5471 master guide, part e: Ownership and transaction reporting

Parts C and D covered the numbers: income, balance sheet, foreign tax credits, and the two anti-deferral regimes. Part E covers the paper trail behind those numbers. Schedule B identifies who owns the foreign corporation. Schedule J tracks its full accumulated earnings and profits history. Schedule O captures the year’s ownership transactions. Schedule P follows the earnings that have already been taxed once, so they are not taxed again when they actually get distributed.

Schedule B: identifying the shareholders

A quick note before the mechanics: if any person, including the filer, is both a U.S. shareholder and a direct shareholder of the foreign corporation, their information belongs in both Part I and Part II.

Part I is completed by Category 3 and 4 filers, covering U.S. persons who owned, at any time during the annual accounting period and directly or indirectly through foreign entities, 10% or more of combined voting power or 10% or more of total value. Column (e) captures each shareholder’s allocable percentage of the foreign corporation’s Subpart F income. A filer who is both Category 3 and Category 5 because of the section 953(c)(1)(A) related person insurance rules uses a different test here: ownership on the last day of the foreign corporation’s tax year, of any amount of stock, rather than the 10% at-any-time test.

Part II is completed by Categories 1a, 1c, 3, 4, 5a, and 5c, and reports direct shareholders rather than the 10% threshold group. Where a CFC is owned through a foreign disregarded entity, both the FDE and its regarded owner get listed, with the owner’s name in parentheses after the FDE’s name. Which direct owners get listed depends on the category: Category 4 filers list all direct owners of the CFC; Categories 1a, 3, and 5a list the direct owners through which the filer indirectly owns the corporation under section 958(a)(2); Categories 1c and 5c list the direct owners from which the filer’s ownership is attributed under section 958(b).

Schedule J: the corporation’s full earnings and profits history

Schedule J tracks a CFC’s accumulated earnings and profits, and, for limited purposes under section 965(e)(2), an SFC’s as well. Categories 1a, 4, and 5a file it. Before the numbers, two identifying items: line a asks for the separate category of income (using the same category codes drawn from the Form 1118 instructions that show up on Schedule E), and line b asks for a country code if the category on line a is the section 901(j) sanctioned country category.

Part I organizes accumulated E&P into columns that track its origin and vintage. Column (c) is pre-1987 earnings not previously taxed. Column (d) is hovering deficits and the deduction for suspended taxes, relevant when E&P and foreign tax credits carry over in certain foreign to foreign nonrecognition transactions under section 381 and one of the merging corporations had a deficit going in. Column (e) is previously taxed earnings and profits, broken into ten sub-columns that mirror the PTEP group structure used throughout the form. Column (f) is the total, the sum of post-2017 earnings not previously taxed, post-1986 undistributed earnings, pre-1987 earnings not previously taxed, and PTEP.

There is a checkbox at the top of Part I for when the filer does not have all U.S. shareholders’ information needed to complete an amount in column (e). Treat checking that box as a last resort rather than a convenience: it is a visible gap in the return that invites exactly the kind of scrutiny you do not want.

Two mechanical rules matter every year. Line 1a’s beginning balances must equal the prior year Schedule J’s ending balances exactly; any discrepancy goes on line 1b with an attached explanation. And where a foreign corporation has more than one applicable income category, the filer completes a separate Schedule J for each category, plus one additional Schedule J coded “TOTAL” that aggregates every line and column across all of them.

The PTEP mechanics running through column (e) trace back to section 959, which sorts previously taxed earnings into the four foreign tax credit baskets under section 904(d) and applies ordering rules to distributions, generally last in, first out within each annual PTEP account, with earnings tied to section 965 given priority treatment. Getting the categorization right here is what keeps a later distribution from being taxed twice.

Schedule O: the year’s ownership activity

Schedule O has a narrower audience than most schedules. Category 2 filers complete Part I. Category 3 filers complete Part II. Nobody else touches it.

Part I, completed by the U.S. officer or director who is the Category 2 filer, reports basic shareholder acquisition information: the shareholder’s name, address, and identifying number, the date they first acquired 10% or more of the corporation, and the date of any later acquisition that added to that position.

Part II breaks into sections. Section A collects general shareholder information: name, address, and identifying number, details of the shareholder’s most recently filed U.S. income tax return, and the date, if any, they last filed a Form 5471 under section 6046 with respect to this same foreign corporation. Section B covers the corporation’s U.S. officers and directors by name, address, Social Security number, and role. Section C reports stock acquisitions: shareholder name, class of stock, acquisition date, method of acquisition (purchase, gift, bequest, trade, and so on), the number of shares acquired directly, indirectly, and constructively, the amount paid, and who the shares were acquired from. Section D mirrors that structure for dispositions: date, method, shares disposed of by category, amount received, and who the shares went to. Section E covers organization or reorganization of the foreign corporation itself: the transferor’s name, address, and identifying number, the transfer date, a description of the assets transferred along with fair market value and, if the transferor was a U.S. person, adjusted basis, and a description of whatever the foreign corporation issued in exchange. Section F rounds out the picture: whether the foreign corporation or a predecessor U.S. corporation filed a U.S. return in the last three years, any reorganizations in the last four years, and, where the corporation sits inside a chain of ownership, an attached chart showing its position and the ownership percentages at each link.

Schedule P: tracking previously taxed earnings and profits

Schedule P exists to prevent double taxation. Once a U.S. shareholder has picked up income under Subpart F, NCTI, or section 965, whether or not the CFC actually distributed anything that year, that income becomes previously taxed earnings and profits. Schedule P is the ledger that follows those earnings so that when the CFC later makes an actual distribution, the portion that traces back to already taxed income is not taxed again.

Categories 1a, 1b, 4, 5a, and 5b file it, generally one per applicable income category. Part I reports PTEP in the CFC’s functional currency; Part II reports the same information translated into the shareholder’s U.S. dollar basis, which is what actually gets used to compute any section 986(c) foreign currency gain or loss when the exchange rate at distribution differs from the rate that applied when the income was originally included. Columns (a) through (k) track the PTEP account’s opening balance, the year’s additions and reductions, and the closing balance, following the same ordering logic described under Schedule J: PTEP splits across the section 904(d) baskets, distributions draw from the most recent annual account first, and section 965 related PTEP gets priority treatment ahead of the general ordering rule.

Coming up in part f

Part F closes out the series with the penalty structure under sections 6038 and 6046, the correction process for a return filed wrong, the summary procedure available for dormant foreign corporations, and the extended statute of limitations under section 6501(c)(8) that keeps an entire return open when an international information return is missing or incomplete.

Sources for this article: IRS Instructions for Form 5471 (Rev. 12/2025), Schedule B section (primary text); IRC §§381, 901(j), 904(d), 951(a), 953(c)(1)(A), 958(a)-(b), 959, 965(e)(2), 986(c), 6046; Treasury Regulations §§1.6046-1(c)(4)(ii), 1.960-3(c)(2). Schedule J, O, and P structural detail in this article, where not drawn directly from the instructions, is cross-checked against multiple independent professional summaries of the current form; treat the granular column references as a strong orientation rather than a substitute for the line-by-line instructions when preparing an actual filing.

Form 5471 master guide: complete IRS filing reference for 2026, by Brolma Advisory

A six part Form 5471 guide built entirely from IRS instructions, the Internal Revenue Code, and Treasury Regulations. Filing categories, CFC ownership, Subpart F, NCTI, penalties, and more.

Part A: Who must file and when

Part B: Constructive ownership and CFC status

Part C: The financial schedules

About Brolma Advisory

Brolma Advisory is an accounting, tax, and financial advisory firm built for businesses and individuals whose situations do not fit standard templates. We work with international businesses establishing or operating in the United States, US companies expanding abroad, and complex businesses including SEC reporting and public company close support, multi-entity and intercompany structures, tech and SaaS platforms, subscription and recurring revenue models, and e-commerce and platform sellers. On the individual side, we advise UK and US professionals, founders, and investors navigating both tax systems, along with US expats living and working abroad.

What connects all of it is complexity that generic accounting was never built to handle. Cross border ownership, deferred revenue, multi-currency reporting, entities with non-US owners, cash and revenue that never quite line up. Brolma Advisory builds accounting and tax structures that reflect how these businesses actually work, so the numbers make sense and the compliance holds up wherever it is tested.

Disclaimer:

Content published by Brolma Advisory is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Brolma Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@brolma.com

Brolma Advisory

941 W Morse Blvd suite 100

Winter Park

Florida

32789