Form 5471 master guide: Form 5471 penalties and the extended statute of limitations

What happens when Form 5471 is filed late, wrong, or not at all, including the section 6501(c)(8) extended statute of limitations. Part F of the Brolma Advisory Form 5471 Master Guide.

5471 GUIDE

7/18/20267 min read

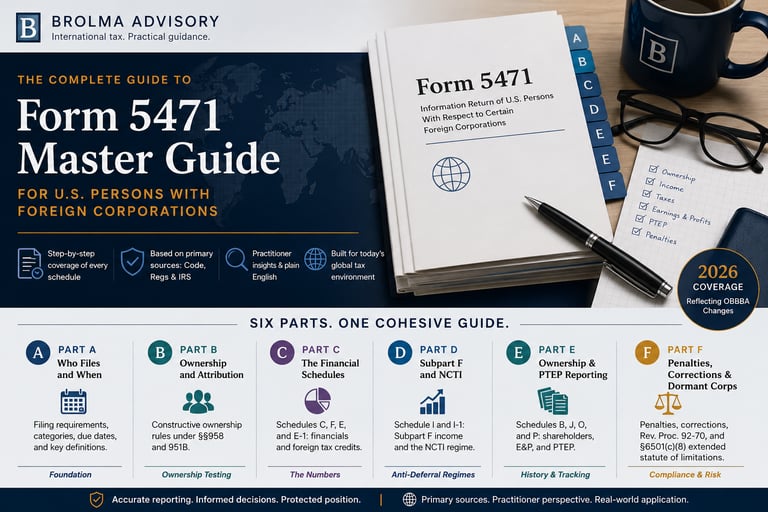

Form 5471 master guide, part f: Penalties, corrections, and dormant corporations

This closes out the series, and it covers the part of Form 5471 that makes everything in Parts A through E worth getting right the first time. The penalty structure is unforgiving by design, a missed or incomplete filing can leave an entire tax return open to audit indefinitely, and the two relief provisions that soften this, the dormant corporation shortcut and the reasonable cause exceptions, only help if you know they exist before you need them.

The section 6038 penalty structure

Failing to furnish the information required under section 6038(a) within the prescribed time triggers a $10,000 penalty for each annual accounting period of each foreign corporation. If the information still is not filed 90 days after the IRS mails a notice of the failure, an additional $10,000 penalty applies for each 30-day period, or part of one, that the failure continues, capped at $50,000 in additional penalties per failure. That puts the maximum civil penalty per foreign corporation per year at $60,000 before any interest.

There is a second, separate consequence layered on top: a 10% reduction of the foreign taxes available for credit under sections 901 and 960. If the failure continues 90 days or more past the IRS notice, an additional 5% reduction applies for each 3-month period the failure continues, subject to the overall limits in section 6038(c)(2).

Both penalties have a genuine escape hatch. Regulations sections 1.6038-1(j)(4) and 1.6038-2(k)(3) provide for alleviation in certain cases, and this is where a documented reasonable cause argument, not just a general appeal to the complexity of the form, actually matters.

The section 6046 penalty structure

Schedule O failures run on a parallel but separate track under section 6679. Failing to file or report all information required under section 6046 triggers a $10,000 penalty for each failure, for each reportable transaction, with the same 90-day notice period and $10,000 per 30-day period escalation, capped at $50,000 in additional penalties.

Criminal exposure

Sections 7203, 7206, and 7207 can apply to failures involving Form 5471, covering willful failure to file, filing false statements under penalty of perjury, and delivering fraudulent documents to the IRS respectively. These require a level of intent well beyond the civil penalty triggers, but they exist, and a client who has been deliberately concealing an interest in a foreign corporation is in materially different territory than one who simply missed a filing category.

One structural point worth flagging for anyone using the joint filing exception from Part A: if you are the person required to file and you arrange for someone else to file Schedule J, M, or O on your behalf, you can still be on the hook for these penalties if that other person’s filing turns out to be incorrect or incomplete. Delegating the filing does not delegate the liability.

Adjacent penalty provisions worth knowing

Section 6662(j) imposes penalties for undisclosed foreign financial asset understatements, with its own reasonable cause and good faith exception under sections 6662(j) and 6664(c). Separately, Rev. Proc. 2019-40 section 7 waives certain section 6038 and 6662 penalties for filers who qualify for the alternative information relief described in Part A.

Beyond Form 5471 itself, a reportable transaction connected to a CFC can trigger a Form 8886 disclosure obligation, covering five categories: listed transactions, confidential transactions meeting the applicable advisor fee threshold, transactions with contractual protection against disallowance, loss transactions meeting the applicable taxpayer specific threshold (the thresholds differ materially by filer type, corporations sit at a much higher dollar amount than individuals, trusts, and most partnerships, with a separate lower threshold for section 988 foreign currency losses), and anything the IRS specifically identifies as a transaction of interest. Missing that disclosure brings its own penalty under section 6707A, separate from anything tied to Form 5471 directly. Material advisors face a parallel Form 8918 disclosure obligation.

The extended statute of limitations under section 6501(c)(8)

This is the provision that turns a single missed filing into a multi year problem, and it deserves to be understood on its own rather than folded into the general penalty discussion, because it is not really a penalty. It is a suspension of the IRS’s clock.

Under normal rules, section 6501(a) gives the IRS three years from the filing date to assess additional tax. Section 6501(c)(8) overrides that for any tax year connected to a required international information return, including Form 5471, that was not filed or was filed incomplete or inaccurate. In that situation, the assessment period does not begin to run until the correct information is actually furnished to the IRS, and then continues for three more years from that date. Critically, the default rule extends to the entire tax return for that year, not just the items connected to the missing Form 5471. A single overlooked Category 5 filing can, in principle, keep every item on that year’s return open to adjustment indefinitely.

Section 6501(c)(8)(B), added in 2010, narrows this considerably where the filer can show the failure was due to reasonable cause and not willful neglect. In that case, the extended period applies only to the items related to the failure, not the entire return. This is the single strongest reason to document a reasonable cause position contemporaneously rather than reconstructing one later: the difference between the two outcomes is the difference between a bounded exposure and an unbounded one.

Correcting a Form 5471 that was filed wrong

If a previously filed Form 5471 turns out to be incomplete or incorrect, the fix is a corrected Form 5471 attached to an amended return, filed using the amended return procedures that apply to whatever return the original Form 5471 was attached to. Write “Corrected” at the top of the form and attach a statement identifying exactly what changed. There is no separate standalone correction process independent of amending the underlying return.

Dormant foreign corporations: the Rev. Proc. 92-70 shortcut

Not every foreign corporation with a filing obligation is actually doing anything. Rev. Proc. 92-70 gives genuinely inactive corporations a real break, provided the corporation meets every one of the following at all times during its annual accounting period: it conducted no business and owned no stock in anything other than another dormant foreign corporation; no shares beyond directors’ qualifying shares were sold, exchanged, redeemed, or transferred, and the corporation was not party to a reorganization; no assets were sold, exchanged, or transferred beyond de minimis amounts; gross income and gross expenses were each no more than $5,000; the value of its assets under U.S. GAAP, without reduction for liabilities, did not exceed $100,000; no distributions were made; and current or accumulated earnings and profits were either zero or changed only by de minimis amounts tied to the limited activity permitted above.

A corporation that clears all of those bars can use the summary filing procedure: complete only page 1 of Form 5471, labeled at the top margin “Filed Pursuant to Rev. Proc. 92-70 for Dormant Foreign Corporation,” including the filer’s name, address, identifying number, category, stock ownership percentage, and tax year, plus the corporation’s own name, address, EIN if any, country and date of incorporation, and annual accounting period. File that summary return the same way you would file Form 5471 generally, attached to the filer’s underlying income tax, partnership, or exempt organization return by its due date including extensions; the current instructions no longer call for a separate duplicate copy to be mailed anywhere.

Using the procedure correctly satisfies the filing obligations under sections 6038(a)(1), 6038(a)(4), and 6046(a)(3), and shields the filer from the penalties under sections 6038(b)(1), 6038(c), 6679, and 7203 tied to those obligations. It is not a complete shield, though: penalties and foreign tax credit reductions under sections 6038(b)(2) and 6038(c)(1) can still apply if the filer fails to timely furnish additional information the IRS specifically requests under section 4.05 of the revenue procedure. And a genuinely de minimis amount of Subpart F income earned even by a qualifying dormant corporation is still taxable to its U.S. shareholders under sections 951 and 952; the summary procedure simplifies the paperwork, it does not exempt real income from tax.

Closing the series

Six parts, one source discipline: primary IRS instructions, the Internal Revenue Code, Treasury Regulations, and named revenue procedures, fact checked at every step and corrected twice along the way when that checking caught something worth fixing. Form 5471 will keep changing under OBBBA as Treasury issues guidance on sections 958(b)(4) and 951B, as Schedule I-1 gets rebuilt to drop QBAI, and as the Pro Rata Share Transition Rule gets interpreted in practice. This guide is a foundation for that ongoing work, not a substitute for checking IRS.gov/Form5471 before every filing season.

Sources for this article: IRS Instructions for Form 5471 (Rev. 12/2025), Penalties and Dormant Foreign Corporations sections; IRC §§901, 960, 6038, 6046, 6501(a), 6501(c)(8), 6662(j), 6664(c), 6679, 6707A, 7203, 7206, 7207; Treasury Regulations §§1.6038-1(j)(4), 1.6038-2(k)(3); Rev. Proc. 92-70, 1992-2 C.B. 435; Rev. Proc. 2019-40, 2019-43 I.R.B. 982.

Form 5471 master guide: complete IRS filing reference for 2026, by Brolma Advisory

A six part Form 5471 guide built entirely from IRS instructions, the Internal Revenue Code, and Treasury Regulations. Filing categories, CFC ownership, Subpart F, NCTI, penalties, and more.

Part A: Who must file and when

Part B: Constructive ownership and CFC status

Part C: The financial schedules

About Brolma Advisory

Brolma Advisory is an accounting, tax, and financial advisory firm built for businesses and individuals whose situations do not fit standard templates. We work with international businesses establishing or operating in the United States, US companies expanding abroad, and complex businesses including SEC reporting and public company close support, multi-entity and intercompany structures, tech and SaaS platforms, subscription and recurring revenue models, and e-commerce and platform sellers. On the individual side, we advise UK and US professionals, founders, and investors navigating both tax systems, along with US expats living and working abroad.

What connects all of it is complexity that generic accounting was never built to handle. Cross border ownership, deferred revenue, multi-currency reporting, entities with non-US owners, cash and revenue that never quite line up. Brolma Advisory builds accounting and tax structures that reflect how these businesses actually work, so the numbers make sense and the compliance holds up wherever it is tested.

Disclaimer:

Content published by Brolma Advisory is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Brolma Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@brolma.com

Brolma Advisory

941 W Morse Blvd suite 100

Winter Park

Florida

32789